2QFY2019 Result Update | Automobile

November 15, 2018

Ashok Leyland Ltd.

BUY

CMP

`108

Performance Update

Target Price

`149

(` cr)

2QFY19

2QFY18

% yoy 1QFY19

% qoq

Investment Period

12 months

Revenue

7,608

6,047

25.8

6,250

21.7

Stock Info

EBITDA

790

609

29.7

623

26.8

Sector

Automobile

OPM (%)

10.4

10.1

31

10.0

41

Market Cap (` cr)

31,219

Reported PAT

460

334

37.5

370

24.2

Net Debt (` cr)

3,739

Source: Company, Angel Research

Beta

1.1

For 2QFY2019, Ashok Leyland Ltd (ALL) posted good set of results both on top-

52 Week High / Low

168/103

line as well as bottom-line fronts. Revenue grew by 25.8% yoy to `7,608cr. On

Avg. Daily Volume

12,80,187

Face Value (`)

5

the bottom-line front, ALL reported PAT growth of 37.5% yoy to `460cr on the

BSE Sensex

35,110

back of strong top-line growth and operating margin improvement.

Nifty

10,569

Strong volumes boost overall top-line growth: The company’s top-line grew by

Reuters Code

ASOK.BO

25.8% yoy to `7,608cr on the back of strong volume growth (up ~27% yoy).

Bloomberg Code

AL.IN

During the quarter, MHCV segment grew by ~22% and LCV segment grew by

~42%. However, overall realization has declined by ~1% (higher discount given

Shareholding Pattern (%)

by ALL). Further, the growth pace in Q3FY19E is expected to remain slow owing

Promoters

51.1

to liquidity issues, however, post that strong sales growth is expected. The growth

MF / Banks / Indian

5.8

FII / NRIs / OCBs

22.9

will be led by pre-buying sales (due to introduction of BS6 norms FY2020) and

Indian Public/Others

20.2

government’s push for infra & construction projects (around 45% of ALL’s truck

volumes are from the infrastructure and construction segment).

Abs.(%)

3m

1yr

3yr

Strong revenue, healthy operating performance aids profitability: On the

Sensex

(6.6)

6.4

37.2

operating front, the company’s margin rose by 31bps yoy to 10.4%. Moreover,

ALL

(5.3)

5.1

19.6

ALL reported ~38% yoy rise in its net profit to `460cr on the back of strong top-

line growth.

Outlook and Valuation: We expect Ashok Leyland to report net profit (reported)

CAGR of ~21% to ~`2,303cr over FY2018-20E mainly due to improvement in

pre-buying sales (due to introduction of BS6 norms in FY2020) and replacement

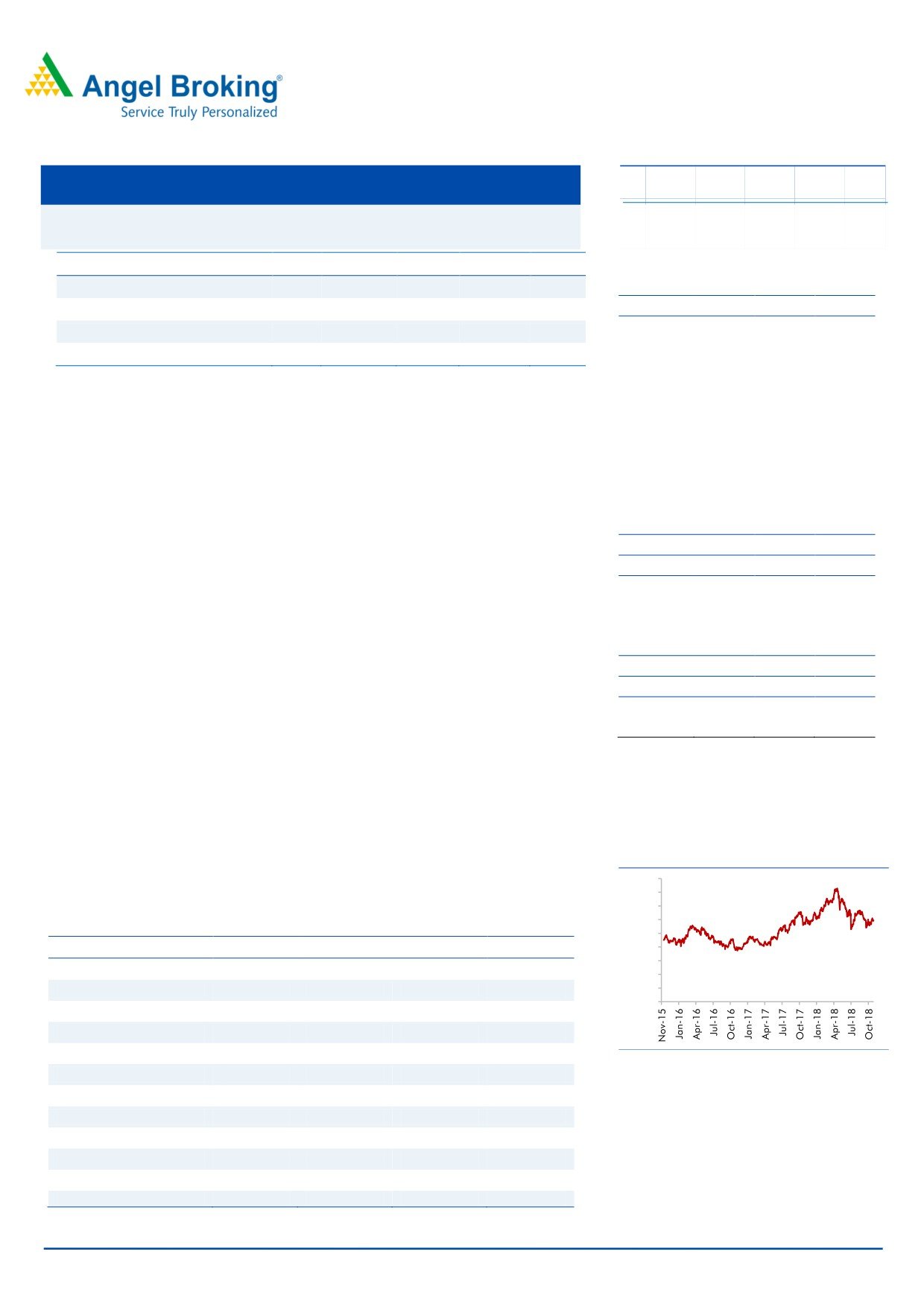

Historical share price chart

demand (implementation of vehicle scrappage policy). Thus, we recommend BUY

180

on the stock with Target Price of `149.

160

140

Key Financials

120

100

Y/E March (` cr)

FY2017

FY2018

FY2019E

FY2020E

80

60

Net sales

20,019

26,248

32,042

37,488

40

% chg

5.7

31.1

22.1

17.0

20

0

Adj. Net profit

1,491

1,571

1,918

2,303

% chg

92.7

5.4

22.1

20.0

EBITDA margin (%)

8.4

9.4

10.3

10.5

Source: Company, Angel Research

EPS (`)

5.1

5.4

6.6

7.9

P/E (x)

21.0

19.9

16.3

13.6

Amarjeet S Maurya

P/BV (x)

5.1

4.4

3.7

3.1

022-40003600 Ext: 6831

RoE (%)

24.3

22.0

22.8

23.0

RoCE (%)

14.0

23.5

29.4

30.5

EV/Sales (x)

1.5

1.0

0.8

0.7

EV/EBITDA (x)

17.7

10.3

8.1

6.5

Source: Company, Angel Research Note

Please refer to important disclosures at the end of this report

1

Ashok Leyland | 2QFY2019 Result Update

Exhibit 1: 2QFY2019 Performance

Y/E March (` cr)

2QFY19

2QFY18

% yoy

1QFY19

% qoq

1HFY19

1HFY18

% chg

Net Sales

7,608

6,047

25.8

6,250

21.7

13858

10334

34.1

Consumption of RM

5529

4,314

28.2

4351

27.1

9,880

7,246

36.4

(% of Sales)

72.7

71.3

69.6

71.3

70.1

Staff Costs

517

492

5.2

493

4.9

1010.4

887.8

13.8

(% of Sales)

6.8

8.1

7.9

7.3

8.6

Other Expenses

772

632

22.1

783

(1.4)

1,551

1,301

19.2

(% of Sales)

10.1

10.5

12.5

11.2

12.6

Total Expenditure

6,818

5,438

25.4

5,627

21.2

12,442

9,434

31.9

Operating Profit

790

609

29.7

623

26.8

1,417

900

57.4

OPM

10.4

10.1

10.0

10.2

8.7

Interest

17

41

(57.7)

12

49.9

29

78

(62.7)

Depreciation

140

141

(0.7)

143

(2.0)

283

273

3.6

Other Income

28

56

(49.4)

53

(47.3)

78

94

(16.9)

PBT (excl. Ext Items)

661

483

36.9

522

26.6

1,182.54

643.13

83.9

Ext (Income)/Expense

-

-

-

-

-

PBT (incl. Ext Items)

661

483

36.9

522

26.6

1,183

643

83.9

(% of Sales)

8.7

8.0

8.4

8.5

6.2

Provision for Taxation

201

148

35.5

152

32.4

353

198

78.5

(% of PBT)

30.4

30.7

29.1

29.8

30.7

Reported PAT

460

334

37.5

370

24.2

829.68

445.50

86.2

PATM

6.0

5.5

5.9

6.0

4.3

Extra-ordinary Items

(16)

(10)

(21)

(8)

Adjusted Profit After Extra-ordinary item

476

334

42.3

380

25.0

850.89

453.27

87.7

Source: Company, Angel Research

November 15, 2018

2

Ashok Leyland | 2QFY2019 Result Update

Outlook and Valuation

We expect Ashok Leyland to report net profit (reported) CAGR of ~21% to

~`2,303cr over FY2018-20E mainly due to improvement in pre-buying sales (due

to introduction of BS6 norms in FY2020) and replacement demand

(implementation of vehicle scrappage policy). Thus, we recommend BUY on the

stock with Target Price of `149.

Downside risks to our estimates

Slowdown in industrial activities could restrict sales volume for ALL.

Delay in implementation of vehicle scrappage policy could restrict the

additional sales growth for company.

Company Background

Ashok Leyland Ltd (ALL) is a holding company. The company is engaged in

commercial vehicles and related components. Through its subsidiaries, it is

engaged in manufacturing and trading in Medium and Heavy Commercial Vehicle

(MHCV), Light Commercial Vehicles (LCV), Passenger Vehicles (PV), automotive

aggregates, vehicle financing and engineering design services. It offers a range of

18 to 80 seater buses under categories such as city application and electric buses.

It offers a range of trucks, which includes long haul trucks, mining and construction

trucks, and distribution trucks. It designs, develops and manufactures defence

vehicles for armed forces. It offers Light Vehicles, which include DOST, PARTNER,

STiLE and MiTR. It offers power solutions for electric power generation, agricultural

harvester combines, earth moving and construction equipment and marine and

other non-automotive applications. It has operations in India, Sri Lanka,

Bangladesh, Mauritius, the Middle East and Africa.

November 15, 2018

3

Ashok Leyland | 2QFY2019 Result Update

Standalone Profit & Loss Statement

Y/E March (` cr)

FY2016

FY2017

FY2018

FY2019E

FY2020E

Net Sales

18,937

20,019

26,248

32,042

37,488

% chg

39.6

5.7

31.1

22.1

17.0

Total Expenditure

17,498

18,341

23,774

28,742

33,552

Raw Material

13,195

13,973

18,621

22,910

26,804

Personnel

1,385

1,543

1,812

2,627

3,074

Others Expenses

2,918

2,825

3,341

3,204

3,674

EBITDA

1,439

1,677

2,474

3,300

3,936

% chg

79.4

16.5

47.5

33.4

19.3

(% of Net Sales)

7.6

8.4

9.4

10.3

10.5

Depreciation& Amortisation

488

518

555

624

680

EBIT

952

1,160

1,919

2,676

3,257

% chg

146.4

21.9

65.5

39.5

21.7

(% of Net Sales)

5.0

5.8

7.3

8.4

8.7

Interest & other Charges

248

155

131

72

60

Other Income

123

326

443

140

140

(% of PBT)

14.8

24.5

19.8

5.1

4.2

Recurring PBT

827

1,330

2,231

2,744

3,337

% chg

86.9

60.9

67.7

23.0

21.6

Tax

437

107

668

851

1,034

(% of PBT)

52.9

8.0

30.0

31.0

31.0

PAT (reported)

390

1,223

1,563

1,893

2,303

Extraordinary Items

(384)

(268)

(9)

(25)

-

ADJ. PAT

774

1,491

1,571

1,918

2,303

% chg

199.5

92.7

5.4

22.1

20.0

(% of Net Sales)

4.1

7.4

6.0

6.0

6.1

Basic EPS (`)

2.6

5.1

5.4

6.6

7.9

Fully Diluted EPS (`)

2.6

5.1

5.4

6.6

7.9

% chg

199.5

92.7

5.4

22.1

20.0

November 15, 2018

4

Ashok Leyland | 2QFY2019 Result Update

Standalone Balance Sheet

Y/E March (` cr)

FY2016

FY2017

FY2018

FY2019E FY2020E

SOURCES OF FUNDS

Equity Share Capital

285

285

293

293

293

Reserves& Surplus

5,123

5,841

6,861

8,107

9,700

Shareholders Funds

5,407

6,126

7,154

8,400

9,993

Total Loans

2,415

2,145

1,002

700

700

Deferred Tax Liability

753

741

726

726

726

Total Liabilities

8,575

9,012

8,882

9,826

11,419

APPLICATION OF FUNDS

Gross Block

5,279

5,858

6,312

6,958

7,658

Less: Acc. Depreciation

487

887

1,338

1,962

2,641

Net Block

4,792

4,971

4,974

4,996

5,017

Capital Work-in-Progress

76

206

401

401

401

Investments

1,980

2,879

5,803

2,774

2,774

Current Assets

5,925

5,744

5,408

10,496

13,901

Inventories

1,625

2,501

1,710

2,897

3,697

Sundry Debtors

1,251

860

980

1,931

2,465

Cash

1,593

912

1,004

2,624

3,802

Loans & Advances

712

709

1,120

1,602

2,062

Other Assets

745

762

593

1,442

1,874

Current liabilities

4,623

5,402

8,131

8,801

10,249

Net Current Assets

1,303

342

(2,723)

1,695

3,652

Deferred Tax Asset

424

614

427

427

427

Mis. Exp. not written off

-

-

-

-

-

Total Assets

8,575

9,012

8,882

9,826

11,419

November 15, 2018

5

Ashok Leyland | 2QFY2019 Result Update

Standalone Cashflow Statement

Y/E March (Rs cr)

FY2016

FY2017

FY2018

FY2019E FY2020E

Profit before tax

390

1223

1563

2744

3337

Depreciation

488

518

555

624

680

Change in Working Capital

(179)

190

2962

(2799)

(778)

Interest / Dividend (Net)

203

88

77

0

0

Direct taxes paid

(441)

(348)

(415)

(851)

(1034)

Others

1223

484

677

0

0

Cash Flow from Operations

1683

2155

5418

(281)

2204

(Inc.)/ Dec. in Fixed Assets

34

(366)

(532)

(500)

(700)

(Inc.)/ Dec. in Investments

330

(1111)

(2800)

3028

0

Cash Flow from Investing

364

(1477)

(3332)

2528

(700)

Issue of Equity

0

0

0

0

0

Inc./(Dec.) in loans

(789)

(883)

(1270)

(302)

0

Dividend Paid (Incl. Tax)

(154)

(325)

(549)

(325)

(325)

Interest / Dividend (Net)

(263)

(151)

(175)

0

0

Cash Flow from Financing

(1205)

(1359)

(1994)

(628)

(325)

Inc./(Dec.) in Cash

842

(681)

92

1619

1179

Opening Cash balances

751

1593

912

1004

2624

Closing Cash balances

1593

912

1004

2624

3802

November 15, 2018

6

Ashok Leyland | 2QFY2019 Result Update

Exhibit 2:

Y/E March

FY2016

FY2017

FY2018

FY2019E FY2020E

Valuation Ratio (x)

P/E (on FDEPS)

40.5

21.0

19.9

16.3

13.6

P/CEPS

35.7

18.0

14.8

12.4

10.5

P/BV

5.8

5.1

4.4

3.7

3.1

Dividend yield (%)

0.5

1.0

0.0

0.0

0.0

EV/Sales

1.6

1.5

1.0

0.8

0.7

EV/EBITDA

21.0

17.7

10.3

8.1

6.5

EV / Total Assets

3.5

3.3

2.9

2.6

2.1

Per Share Data (Rs)

EPS (Basic)

2.6

5.1

5.4

6.6

7.9

EPS (fully diluted)

2.6

5.1

5.4

6.6

7.9

Cash EPS

3.0

5.9

7.2

8.6

10.2

DPS

0.5

1.1

0.0

0.0

0.0

Book Value

18.5

20.9

24.4

28.7

34.1

Returns (%)

ROCE

12.2

14.0

23.5

29.4

30.5

Angel ROIC (Pre-tax)

22.4

25.9

142.2

72.3

79.1

ROE

14.3

24.3

22.0

22.8

23.0

Turnover ratios (x)

Asset Turnover (Gross Block)

3.6

3.4

4.2

4.6

4.9

Inventory / Sales (days)

31

46

24

33

36

Receivables (days)

24

16

14

22

24

Payables (days)

50

56

66

60

60

Working capital cycle (ex-cash) (days)

6

5

(29)

(5)

0

Source: Company, Angel Research

November 15, 2018

7

Ashok Leyland | 2QFY2019 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited, Bombay

Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager and Investment Adviser with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking

Limited is a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration

number INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for

accessing /dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed

public offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Disclosure of Interest Statement

Ashok Leyland

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to -15%)

Sell (< -15%)

November 15, 2018

8